MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles. The below article originally appeared in Tim Ingham’s latest MBW+ Review email, issued exclusively to MBW+ subscribers last week.

Socialist French politician Aurore Lalucq is the co-founder of Tax The Rich, which wants to raid the assets of wealthy individuals to fund “climate transition” in Europe.

She’s also called for the magical deletion of over $2.5 trillion (!!) in Eurozone government debt from the books of the European Central Bank.

Politically speaking, she’s AOC as an MEP.

Now, Universal Music Group is in her crosshairs.

On April 4, Lalucq called on EU competition chiefs to scrutinize Universal’s proposed $775 million acquisition of Downtown Music Holdings, suggesting that it might gift UMG “unprecedented control over routes to market”.

Her comments were cheered by indie label group IMPALA, which is looking to snowball momentum against UMG’s Downtown deal in Europe. IMPALA claims that UMG’s buyout of Downtown – following the major’s recent buys of [PIAS] and 8Ball – will enable it to “gatekeep market access”.

Despite these protestations, I predict UMG’s buy of Downtown will breeze through without regulatory intervention worldwide – and not just because of today’s Trump–influenced, anything-goes business environment.

Here’s why…

1) Universal is far from a monopoly

Market share sizing is always a dangerous game in the music business, so let’s keep this simple.

According to IFPI, the trade revenues of the global recorded music rights industry (i.e. sales plus streams plus music licensing) amounted to USD $29.6 billion in 2024.

Universal Music Group’s reported turnover from the same income sources last year hit EUR €8.90 billion, equivalent to USD $9.63 billion.

That’s a global market share, on a trade revenue basis, of around 32.5%.

By my estimates, using data from UMG’s latest annual report and IFPI figures, Universal’s market share in North America last year sat at around 42%. In Europe (including the UK), it was closer to 31%.

These numbers are simply not large enough to trigger monopoly concerns.

In the US, the Federal Trade Commission states that antitrust courts typically need to see a company own a market share of 50% or above to even consider if it exercises “monopoly power”.

Meanwhile, the European Commission says, “If a company has a market share of less than 40%, it is unlikely to be dominant.”

Universal Music Group is comfortably below these thresholds, and the addition of Downtown brings no danger that it will exceed them.

(UMG’s market share in Asia and Latin America is considerably lower than its equivalents in the US and Europe – which is why I’ve predicted a raft of M&A activity from the company in these regions in the years ahead.)

2) Independent music ownership is thriving

Whose side are you on: David or Goliath?

This is an age-old argument from indie label reps when trying to hobble major music company expansion.

But in the modern age, things get complicated.

Universal Music Group is already paying out ten-figure sums annually to copyright-owning artists and independent labels as their distribution/services partner. (UMG mainly delivers these royalties via Virgin Music Group.)

So, sure, if you like, it’s David vs. Goliath.

But only if Goliath’s pockets are stuffed with envelopes of cash – destined for the letterboxes of David’s fellow indie villagers.

This brings us to the strongest argument for Universal’s Downtown acquisition to pass regulators: in music, there is a crucial difference between ‘distributed‘ market share and ‘owned’ market share.

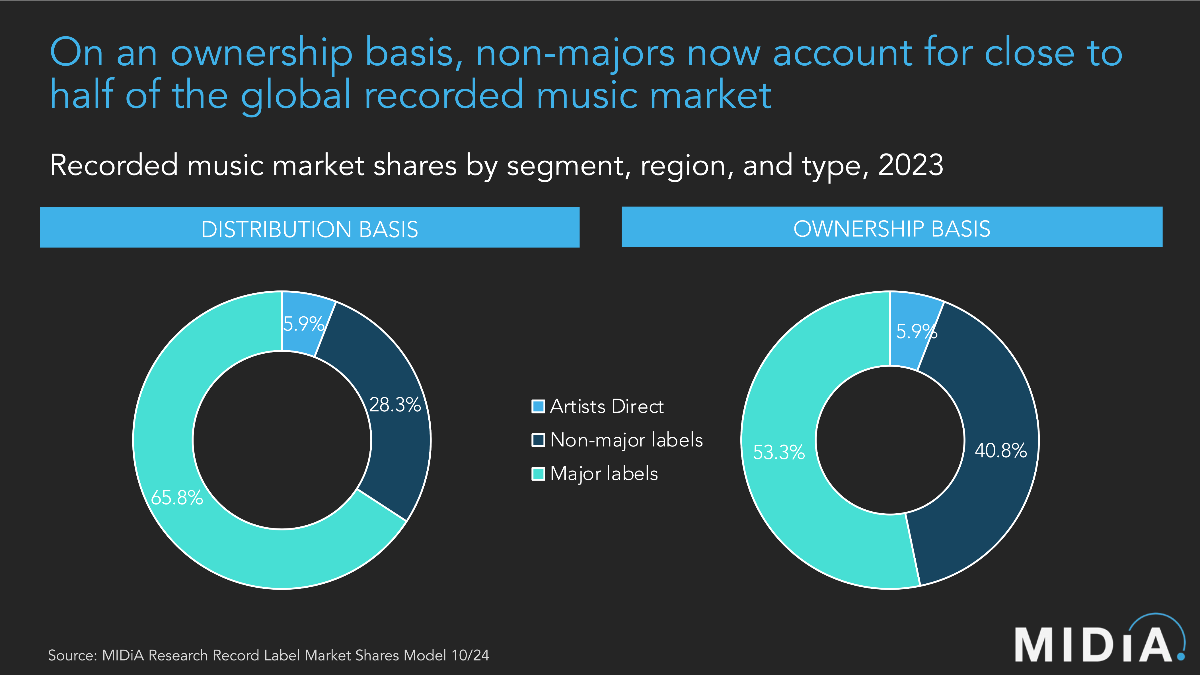

According to Midia Research, the three ‘majors’ (Universal, Sony, and Warner) jointly claim around 66% of global recorded music trade revenues on a distribution basis, leaving the indies with just 33%.

Yet on a copyright-ownership basis, independent artists/labels claim a whopping 47% of the worldwide market.

Midia’s numbers imply that around 20% of recorded music revenue at the three major music companies is collected on behalf of copyrights they don’t own.

In UMG’s case, in 2024, that ~20% would have equated to nearly USD $2 billion.

Once collected, UMG would have paid the majority of this money back to indie distribution clients.

In buying Downtown, Universal is acquiring a company with zero owned copyrights. (Downtown sold its music copyright catalog to Concord for $400 million a few years back, after which it transformed into a ‘pure service’ business working on behalf of indie artists, songwriters, and labels.)

So not only will the addition of Downtown only cause a minor percentage shift in UMG’s global distribution market share, it will actually have zero impact on UMG’s market power as a copyright owner.

3) Independent music distribution is thriving

In light of the above, IMPALA is careful to argue that – following its acquisition of Europe-based distributor [PIAS] last year – UMG’s buyout of Downtown will lead to unfair concentration in music distribution.

Yet even this is detached from the reality.

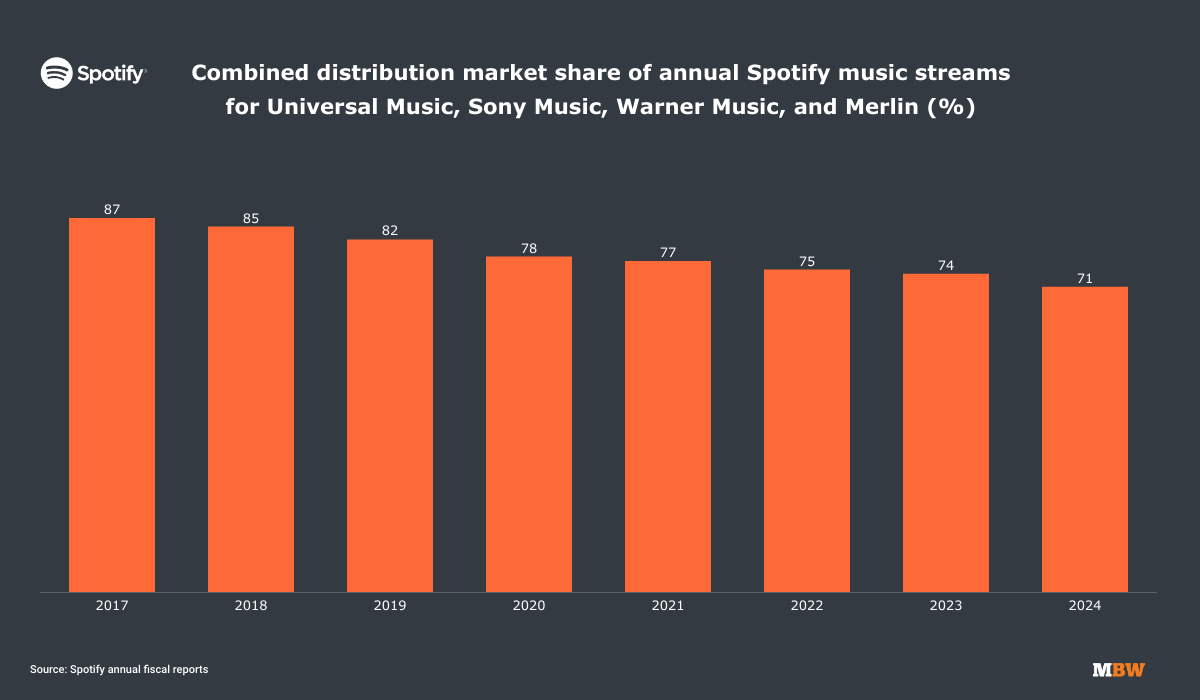

Those who like to see the majors get a kicking often point to the chart below, which shows how the majors’ distribution market share, plus that of indies repped by Merlin, has fallen by double-digits on Spotify over the past decade.

This major-market-share decline has predominantly been driven by two factors:

(i) The huge jump in consumption of independent artist/label music in markets like Europe, MENA, India, Latin America, and South Korea; and

(ii) The emergence of strongly monetized, self-distributing companies outside of the majors – from Believe to EMPIRE, Create Music Group, and gamma. (All of whom, by the way, are either worth, or have raised, in excess of a billion dollars.)

Two of the largest music companies in the world, BMG and Concord, are also now capable of self-distribution: BMG via its direct relationship with Spotify and Apple, and Concord via its recent acquisition of Stem.

The point? Not only is Universal now paying out billions to indies annually as a distribution partner, but those indies (a) have complete freedom to leave UMG and move their catalogs elsewhere, and (b) have a plethora of powerful competitors to choose from – that stretch far beyond Downtown.

Some in the indie sector have raised particular concerns over the fact that, by acquiring Downtown, Universal will also take ownership of FUGA, a B2B content delivery platform, and Curve, a royalty processing platform. Both have direct relationships with many key independents.

But here, too, you’ll find strongly monetized competitors: Audio Salad, for example, rivals FUGA, and is owned by SESAC/Blackstone. Meanwhile, Tone – originally part of Stem – competes with Curve and has been backed by billionaire Jack Dorsey’s Block Inc.

4) Universal’s EMI acquisition in 2012/2013 didn’t create an almighty monopoly, after all. In fact, EU regulators probably got it wrong.

Thirteen years ago, egged on by outraged independent music lobbyists, Europe’s regulators dramatically failed to predict the modern world. A world in which Universal – and its thirty-something-percent global market share – battles an onslaught of formidable independent distribution rivals.

In 2012, said watchdogs forced Universal Music Group to divest a vast chunk of catalog from its USD $1.9 billion acquisition of EMI Music. (This divestment became Parlophone Label Group, which Warner bought the following year for around USD $765 million.)

In doing so, the European Commission swallowed arguments that the EMI deal would further UMG’s “monopolistic position” in music, and would lead to Universal gaining an invulnerable market share of over 50% in key territories like the UK.

Wrong, wrong, wrong.

In fact, thanks to strong competition and the rapid globalization of music streaming, Universal has ended up controlling a smaller piece of a much larger worldwide market.

Music & Copyright data suggests that in 2013, fresh from its EMI acquisition, UMG’s global distribution market share hit its peak at 39.7%.

Ten years later, in 2023, thanks to the rise and rise of non-major distribution, that number had fallen to 32.4%.

These statistics should embarrass Europe’s regulators, highlighting their lack of foresight into where the music market was really headed during that 2012/2013 EMI Music acquisition process.

It’s a compelling, data-driven argument: Europe’s demand that UMG divest Parlophone Label Group in 2013 was an act of misguided regulatory overreach, led by doom-mongering forecasts that – we now know – were wildly inaccurate.

I’d expect regulators to be doubly dubious of the same arguments this time around.

Music Business Worldwide