Berkshire Hathaway(NYSE: BRK.A)(NYSE: BRK.B) has produced amazing returns for long-term investors under Warren Buffett’s leadership. However, at a more than $1 trillion valuation, its ability to consistently generate outsize returns from here is somewhat limited.

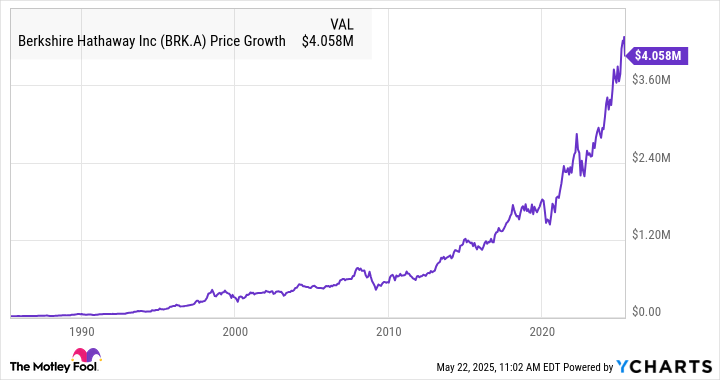

To put Berkshire’s success into perspective, if you had invested $10,000 in Berkshire Hathaway 40 years ago in 1985, you would have nearly $4.1 million today. And that’s if you had bought shares two decades after Warren Buffett took the reins and started building the company into what it is today.

Of course, Berkshire’s long-term track record will be tough to match. But there are a few companies that have some of the right components in place to grow into a much larger value-creation machine like Berkshire, and here are three in particular that are worth a closer look right now.

The most obvious “early Berkshire Hathaway” is specialty insurance company Markel(NYSE: MKL), which is roughly 2% of Berkshire’s size by market cap and uses a similar business model.

Image source: The Motley Fool.

At the core is Markel’s insurance business, and its focus on specialty insurance gives it the potential for superior profitability. There’s also Markel Ventures, which acquires entire operating businesses, and because of the company’s relatively small size, it doesn’t need to make billion-dollar acquisitions to potentially move the needle. After all, Buffett has said many times that his biggest obstacle to finding great and meaningful targets is Berkshire’s massive size.

Then there is Markel’s third focus, which is a portfolio of publicly traded stocks, the top holding in which happens to be Berkshire Hathaway. So all three parts of the business are similar in nature to how Berkshire is structured.

Markel’s recent results have been strong, and there’s a solid case to be made that the stock is undervalued. Over the past five years, Markel’s intrinsic value has grown by nearly 130% but the stock is up by less than half of that amount. Management is in the process of a strategic review to optimize the business, so now could be a great time to take a look.

Howard Hughes Holdings(NYSE: HHH) has been around for about 15 years, and its core business is developing master-planned communities, or MPCs. These are large-scale developments that are the size of small cities, with examples of Howard Hughes’ MPC including The Woodlands near Houston and Summerlin in the Las Vegas area.

Recently, billionaire hedge fund manager Bill Ackman has been pushing to take the company in a different direction. While he has believed in the MPC business for a long time (he owned 37% of the company previously), Ackman recently invested an additional $900 million in Howard Hughes and became the company’s executive chairman for the purpose of acquiring entire businesses with the goal of building a “modern-day Berkshire Hathaway.”

It’s unclear exactly what this will look like, and right now all Howard Hughes has is a $900 million war chest, so it’s in the very early stages of conglomerate building. However, what we do know is that the current MPC business and its leadership team will remain as-is, and that Ackman has said that an insurance business will likely play a big role in the future plans.

To be fair, I bought Howard Hughes stock for the MPC business, long before Ackman’s plans were revealed. But this certainly creates some interesting possibilities, and right now retail investors can buy shares for about 35% less than Ackman just did.

One that’s a little less obvious of a choice is Kinsale Capital Group(NYSE: KNSL), an insurance company that focuses on specialty insurance for smaller clients. And the main reason is that Kinsale has a tremendously profitable insurance business that should give it plenty of capital and operational flexibility to invest in more unique ways as the business grows.

Specialty insurance — that is, special situations and hard-to-assess risks — is a tough business. But if you’re good at it, there is lots of money to be made.

Most insurance companies are happy to generate a single-digit profit margin from underwriting and to make the bulk of their money from investment income. But Kinsale is different. The company has a long track record of best-in-class profitability. In fact, in 2024 Kinsale produced a 76.4% combined ratio, which implies an underwriting profit of nearly 24%.

For clarification, Kinsale hasn’t expressed interest in building a true conglomerate with non-insurance subsidiaries. However, management had said that as the company scales and its investment portfolio grows, the team is comfortable taking on more exposure to equities. And the incredible underwriting margins from the insurance business give it flexibility to not have to completely focus on immediate income from its investments.

I completely acknowledge that Kinsale is the least Berkshire-like business on this list. But I also believe that in 10 years, it will have a significantly more Buffett-style approach to its investment strategy.

To be perfectly clear, I don’t think there will ever be another Berkshire Hathaway, at least in the sense that one of today’s emerging conglomerate will produce 5,500,000% total returns (that’s not a typo) over a 60-year period.

However, Berkshire Hathaway uses a very replicable method of conglomerate-building, and it can certainly be used to create outsized returns over the years. So while I don’t think these three will turn a few thousand dollars into millions of dollars, I think all three are excellent businesses, and I own all three in my own stock portfolio.

Before you buy stock in Markel Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Markel Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider whenNetflixmade this list on December 17, 2004… if you invested $1,000 at the time of our recommendation,you’d have $639,271!* Or when Nvidiamade this list on April 15, 2005… if you invested $1,000 at the time of our recommendation,you’d have $804,688!*

Now, it’s worth notingStock Advisor’s total average return is957% — a market-crushing outperformance compared to167%for the S&P 500. Don’t miss out on the latest top 10 list, available when you joinStock Advisor.

Matt Frankel has positions in Berkshire Hathaway, Howard Hughes, Kinsale Capital Group, and Markel Group. The Motley Fool has positions in and recommends Berkshire Hathaway, Howard Hughes, Kinsale Capital Group, and Markel Group. The Motley Fool has a disclosure policy.