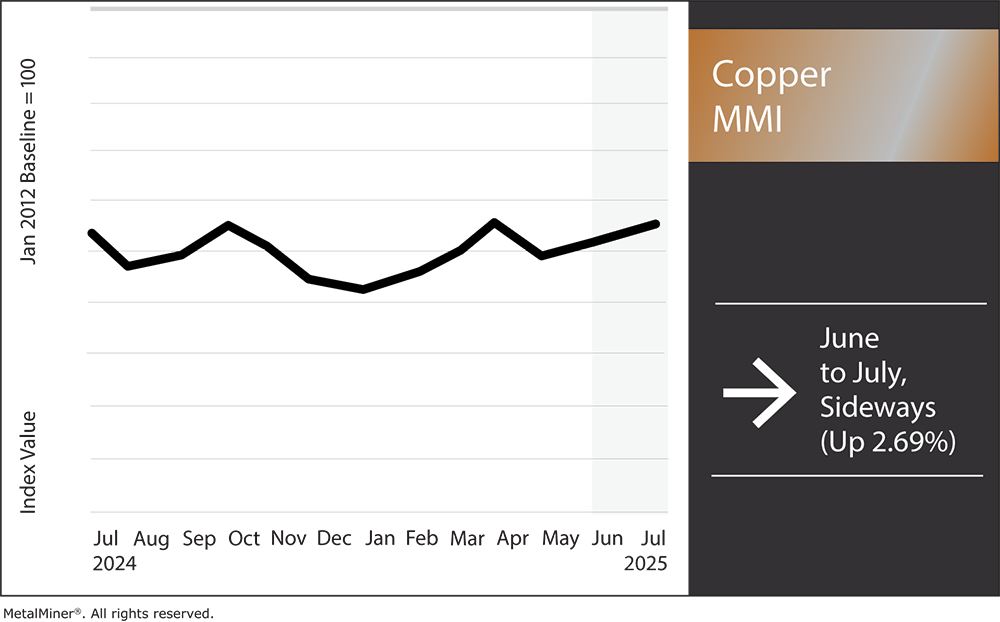

Comex copper prices resumed their uptrend, ending a brief pause witnessed in early June. As of July 7, the price of copper on the exchange stood $266/mt short of its all-time high from late March. This marks an almost 23% rise since the early April low. However, Comex prices aren’t alone. While LME prices remain far short of the all-time high reached in May 2024, they have experienced a similar uptrend since early April, rising by over 14%.

With both contracts on the rise, the considerable delta between the two remains intact. Currently, Comex prices sit nearly 16% higher than their LME counterparts. The bifurcated contracts largely reflected expectations of potential U.S. copper tariffs after the investigation into copper imports began in late February. That delta is likely to expand further after President Trump told press on Tuesday he will likely impose a 50% duty on copper. The announcement came bereft of details, including the timing and scope. Since it was not formalized, the duty rate could change.

U.S. copper tariff threats have offered strong support to the market. That said, this mostly applies to Comex prices, hence their considerable premium over LME. U.S. buyers spent most of the first half filling stocks free of tariffs to hedge against the threat of a potential duty. As a result, global copper stocks remain down, but Comex stocks are up.

In fact, they now tower over their LME and SHFE counterparts. As LME stocks deplete and the spot market becomes increasingly tight, LME prices have been forced to rise to compete for material. Meanwhile, the tight spot market pushed the market into backwardation, with spot prices now coming at a premium to their three-month counterparts. Now that the market has more clarity that the duty will actually occur and likely at 50%, buyers will continue to use whatever window they are given to secure material free of tariffs.

As prices climb higher, global warehouse stocks appear increasingly depleted. While the significant price premium has shifted supply toward the U.S., lifting Comex stocks, LME stocks have remained in decline for almost a year.

Souce: MacroMicro

Following the considerable drawdown, mostly Russian material remains. This is heavily sanctioned by the U.S. and less favored among European buyers. Even as the price of copper fluctuates, tight supply remains a longstanding fear within the market as the world pursues electrification efforts.

While this is at least partially the result of the marked growth of China’s copper smelting industry, the raw material market remains tight. Chinese copper smelters are now accepting no processing fees, which miners pay to smelters, a historic low for the industry.

While staggering considering the annual benchmark copper concentrate stood at $88/mt in 2023, the $0 fee is actually better than expected. Chilean miner Antofagasta had previously requested an unprecedented -$15/mt charge, which is not necessarily a bad offer considering spot charges are trending around -$43/mt.

The first half of the year saw the U.S. dollar dropping below long-term support levels, making for its worst performance since 1973. While new tariffs have helped the U.S. dollar stabilize in the past few days, its overall decline offered support for commodity prices like copper, which trade inversely to it.

As the price of copper nears key resistance levels, investors remain focused on economic forecasts. While copper tariff risks have provided a short-term boost to the price of copper, tariffs overall have left the market increasingly concerned about global growth. The Trump administration continues to roll out new tariffs, the latest of which hit key trade partners, including Japan and South Korea. Meanwhile, trade deals have rolled in much more slowly than anticipated.

While some progress has been made with the UK, China and Vietnam, negotiations remain ongoing with the EU, Mexico and Canada. The uncertainty surrounding tariff threats and their long-term risks to U.S. manufacturing demand, particularly as consumers have had to adjust to the sharp increases in inflation witnessed over recent years, suggests that overall global demand conditions will remain a headwind.

Much of what helped copper prices rise in years past, including the sharp but short-lived uptrend that occurred during the first half of 2024, was largely pinned on expectations of green energy development. However, markets like wind energy and EVs have largely disappointed projections.An electric car charging in California

While electrification development isn’t going away, particularly with the advent of data centers, a net-zero world driven by renewables now seems more like a pipe dream. Meanwhile, reports have begun to emerge that China’s EV sector is starting to resemble a bubble. Driven by considerable subsidies to offset its beleaguered property sector, Chinese EV firms have witnessed a rash of closures over recent years.

While it’s true that global inventory stocks remain on a downtrend, stocks overall do not show any near-term signs of becoming empty. Global stocks remain considerably higher than where they have stood in years past, and concerns over supply will continue to incentivize mining. Meanwhile, Chinese copper smelters remain on pace to match record output.

Although the date has yet to be announced, the window for duty-free copper will come to an end. And while tariff threats have offered a short-term lift to markets, their implementation will remove the current incentive for U.S. buyers to refill stocks. Additionally, tariffs will create a higher price floor, which will result in at least some level of demand destruction in the U.S.

Since it has yet to be formally announced, there’s also a chance the current 50% duty could change. If the U.S. decides to lower it, markets would have to unravel their expectations, which would mean a downside risk for prices.